2025 was a year of recalibration, continuing the softness experienced since the fourth quarter of 2024. Rather than a slowdown, this period can be better described…

2025 was a year of recalibration, continuing the softness experienced since the fourth quarter of 2024. Rather than a slowdown, this period can be better described as a collective deep breath as the industry prepares for the next upcycle in the Asian Pacific region.

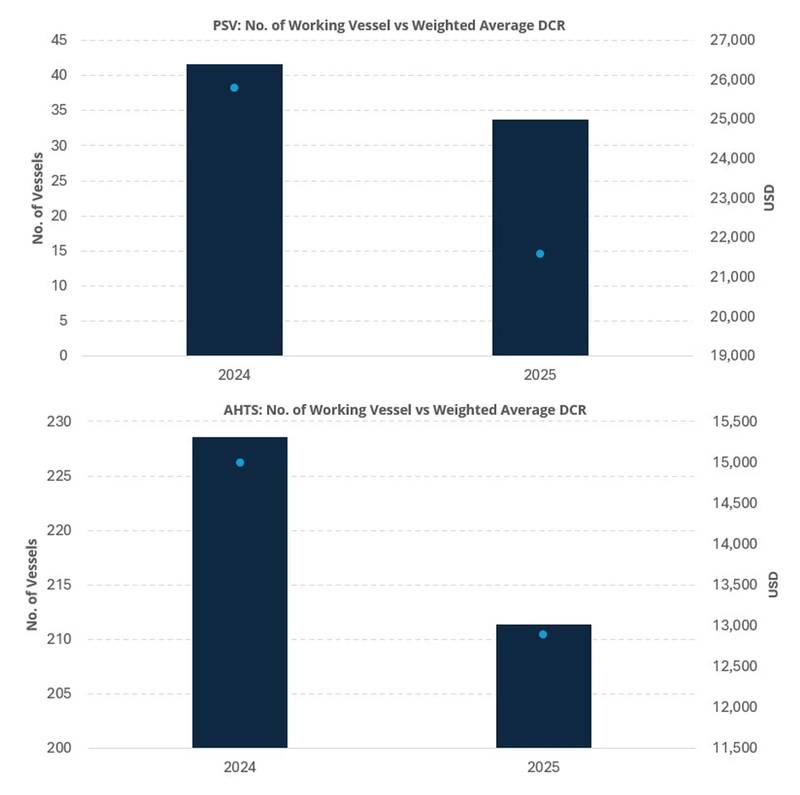

Compared to 2024, the composite dayrates, calculated as a weighted average across size categories, declined by approximately 16% for PSVs and 14% for AHTS vessels. In tandem, utilization also softened, with the number of working vessels down 19% and 8% respectively, a direct reflection of weaker underlying demand.

Across geographies, this theme was evident as global markets cooled from the momentum of earlier strong years. From the waters of Southeast Asia to the coasts of Australia, the industry pressed pause on some of its largest bets with projects such as North Ganal, Lang Lebah, Dorado, and Browse seeing their final investment decisions pushed back from their initial planned dates. On the surface, these headlines may appear negative, but these deferrals have also helped spread out the investment cycle, creating a more balanced pace for the rest of the decade.

© Fearnley Offshore Supply

© Fearnley Offshore Supply

Towards 2028, we expect to see a modest but meaningful uptick

Content Original Link:

" target="_blank">